Compared to variable costing, absorption costing results in higher total product costs and lower net income in periods with lower production volumes. This occurs because fixed overhead costs are allocated across fewer units produced. Absorption costing is a costing method that allocates both variable costs and fixed manufacturing overhead costs to each unit produced. The key difference from variable costing is that fixed manufacturing overhead costs are treated as product costs under absorption costing. Using the absorption costing method on the income statement does not easily provide data for cost-volume-profit (CVP) computations.

Just-In-Time: History, Objective, Productions, and Purchasing

Under absorption costing, all manufacturing costs, both direct and indirect, are included in the cost of a product. Absorption costing is typically used for external reporting purposes, such as calculating the cost of goods sold for financial statements. If absorption costing is the method acceptable for financial reporting under GAAP, why would management prefer variable costing? Advocates of variable costing argue that the definition of fixed costs holds, and fixed manufacturing overhead costs will be incurred regardless of whether anything is actually produced.

How is absorption costing treated under GAAP?

In conclusion, absorption costing and variable costing are two distinct methods of cost allocation that differ in their treatment of fixed manufacturing overhead costs. Absorption costing includes fixed manufacturing overhead costs in the cost of each unit produced and values inventory at a higher level. It can result in higher reported profits when sales volume exceeds production volume. On the other hand, variable costing treats fixed manufacturing overhead costs as period expenses and only includes variable manufacturing costs in the cost of each unit produced. It values inventory at a lower level and provides a clearer picture of profitability.

Why is absorption costing more widely used then variable costing?

The total amount of expenses divided by the number of days gives you the period cost per day. Product and period costs are two of the most crucial cost categories in management accounting. Product costs are directly related to producing a particular good or service, while period costs are not directly related to production but instead occur during a particular period. Thus, we see that variable costing can be extremely useful in several different ways. By understanding the cost behavior of a company and using this information to make informed decisions, businesses can save money and improve their bottom line. This approach can be helpful when making short-term decisions, such as whether to continue producing a product or how to price it.

Absorption Costing vs. Variable Costing: An Overview

Variable costing is more useful than absorption costing if a company wishes to compare different product lines‘ potential profitability. It is easier to discern the differences in profits from producing one item over another by looking solely at the variable costs directly related to production. To conclude this discussion, both absorption and variable costs are commonly used methods of production cost analysis. The major difference between both methods includes the fixed cost as a part of the total cost. Decision making is not as simple as applying a single mathematical algorithm to a single set of accounting data.

- The main difference between the two methods lies in how they treat fixed costs.

- Each is being produced in equal proportion, and the company is fully able to meet customer demand from existing capacity (i.e., producing more will not increase sales).

- Since absorption costing allocates all manufacturing costs to products, it provides a more complete view of product costs.

- Under generally accepted accounting principles (GAAP), U.S. companies may use absorption costing for external reporting, however variable costing is disallowed.

- Absorption costing is not as well understood as variable costing because of its financial statement limitations.

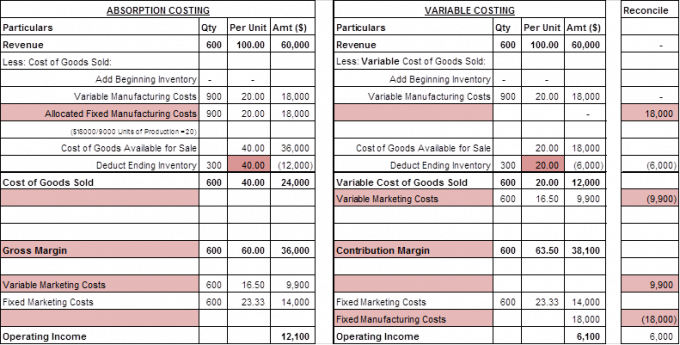

The amount of the fixed overhead paid by the company is not totally expensed, because the number of units in ending inventory has increased. Eventually, the fixed overhead cost will be expensed when the inventory is sold in the next period. Figure 6.13 shows the cost to produce the 8,000 units of inventory that became cost of goods sold and the 2,000 units that remain in ending inventory. Figure 8.1.3 shows the cost to produce the 8,000 units of inventory that became cost of goods sold and the 2,000 units that remain in ending inventory. Variable costing, on the other hand, includes all of the variable direct costs in the cost of goods sold (COGS) but excludes direct, fixed overhead costs. Absorption costing is required by generally accepted accounting principles (GAAP) for external reporting.

Cost accounting is an essential tool for managers, as it provides information that can be used to make decisions about how to allocate resources and run operations. Production is estimated to hold steady at 5,000 units per year, while sales estimates are projected to be 5,000 units in year 1; 4,000 units in year 2; and 6,000 in year 3. In addition, by comparing actual results with budgeted figures, management can assess how well it performs against its goals. No matter which method you choose, it’s essential to be aware of the strengths and weaknesses of each so that you can make the best decision for your business. Production is estimated to hold steady at \(5,000\) units per year, while sales estimates are projected to be \(5,000\) units in year \(1\); \(4,000\) units in year \(2\); and \(6,000\) in year \(3\). In summary, both methods have merits depending on business context and intended use.

Absorption costing is required for external financial reporting under [gaap](/blog/generally accepted accounting principles (GAAP). It provides a fuller allocation of costs for inventory valuation and income determination. Under variable costing, the other option for costing, only the variable production costs are considered.

Even if a company decides to use variable costing in-house, it is required by law to use absorption costing in any external financial statements it publishes. Absorption costing is also the method that a company is required to use stocksfortots for calculating and filing its taxes. Various product and period costs can vary depending on the type of business or organization. Some examples of product costs include direct materials, direct labor, and manufacturing overhead.